How to retire early: 4 strategies to reach financial freedom

So, you want to retire early? You’re not alone: the FIRE (Financial Independence, Retire Early) movement shares the same goal. People in the FIRE community save aggressively and invest wisely to achieve financial independence as quickly as possible. However, while the end goal is the same, there are different strategies to get there.

In this article, we’ll explore four popular approaches to FIRE:

- Regular FIRE

- Lean FIRE

- Fat FIRE

- Barista FIRE

Let’s dive in and discover which path might work best for you!

How to calculate your FIRE number and time to FIRE

Before we begin, let’s talk about the FIRE number. This is the amount of money you need to achieve financial independence and retire early (or “FIRE” in FIRE jargon). To estimate your FIRE number, simply multiply the retirement income you want during your first year of retirement by 25. This is based on the 4% rule.

For example, if your target retirement income is £30,000 in your first year of retirement, you’ll need £750,000 (£30,000 x 25) saved in your FIRE pot before you can retire.

Another key concept in the FIRE movement is time to FIRE. This refers to how long it will take to reach your FIRE number based on how much you’ve already saved and how much you’re saving each month.

Thanks to the power of compounding, even if you save the same amount each month, your money will grow faster the longer you stay invested. You can see this effect clearly using my savings and investments growth calculator.

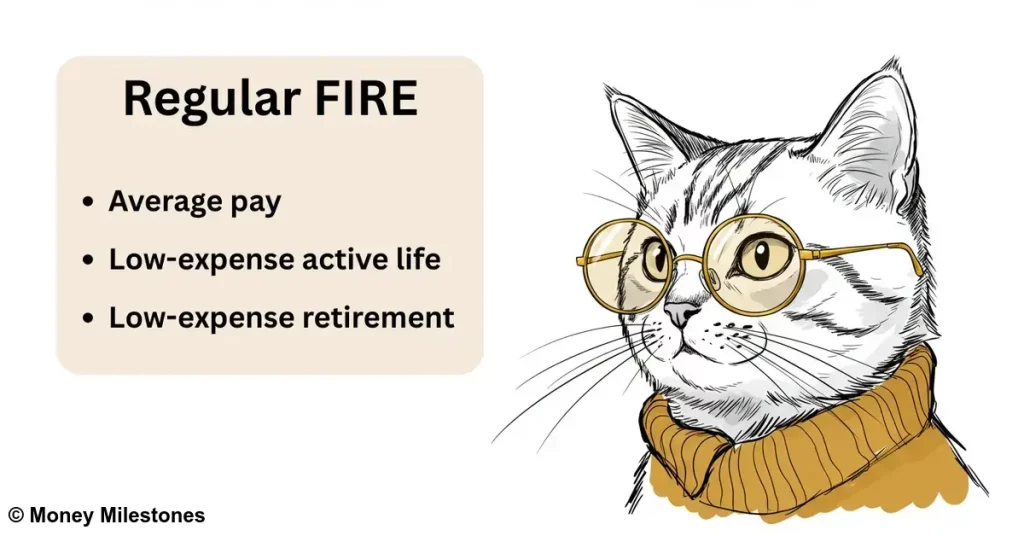

What is Regular FIRE? The original path to early retirement

As explained in my introduction to the FIRE movement, retiring early really comes down to two main things:

- A high savings rate. This means putting aside a large portion of your monthly income. Most FIRE followers recommend saving at least 50%.

- Investing consistently. Historically, investing has been the fastest way to grow your money over time (though growth is never guaranteed). That’s why it’s a key part of the FIRE strategy.

In practice, there are challenges to be aware of. I cover these in more detail in my introduction to the FIRE movement.

How to retire early: A regular FIRE example

Let’s take Paul as an example. He’s 31 and earns the median UK take-home salary of £2,510 per month. He saves 50% of it every month. Paul wants a retirement income of £22,000 per year and already has £50,000 saved in his FIRE pot. This means his FIRE number is £550,000. Assuming his investments grow at 5% per year, Paul will reach his FIRE number in 17.9 years at age 49.

This is the essence of Regular FIRE: it’s the standard path to financial independence for the average earner. But there are also interesting variations on how to achieve FIRE, each following a slightly different route.

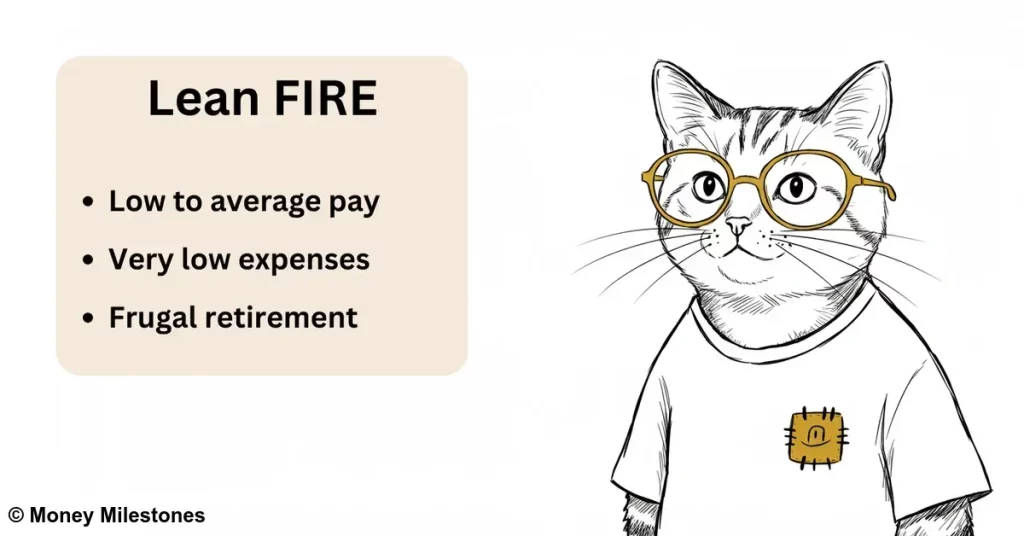

Lean FIRE: How to retire early through a frugal lifestyle

The first path to financial independence at a young age is Lean FIRE. Followers of Lean FIRE value frugality and reject consumerism as a way to achieve early retirement.

They often have low-to-average incomes but make up for it by saving a large portion of what they earn. Because they plan for a modest lifestyle in retirement, their FIRE number is lower, making it easier and quicker to reach.

How to retire early: A lean FIRE example

Let’s illustrate this with an example. Anna, 22, is an office worker earning £2,000 per month after tax. She plans to retire on £1,000 per month, or £12,000 per year. This gives her a FIRE number of £300,000. Assuming she has no savings and saves 50% of her income, her time to FIRE is 16.4 years. With a 5% annual investment growth rate, Anna could retire at age 38 or 39, despite earning an average salary.

This is Lean FIRE in action: even with a low or average income, if you’re willing to live frugally now and in retirement, early financial independence is still possible.

Is lean FIRE right for you? Pros and cons of a frugal early retirement

Lean FIRE might suit you if:

- You earn a low-to-average salary. Your income may not be high, but you’re still able to save every month.

- Your expenses are low. This gives you room to invest a meaningful portion of your income each month (at least 40-50%).

- You’re content with a frugal retirement. You don’t mind living simply in exchange for more freedom.

Lean FIRE probably isn’t for you if:

- You don’t want to watch every penny. If tracking every supermarket trip sounds exhausting, this path might not be for you.

- You want a higher retirement income. For example, if you plan to travel frequently, you’ll need a bigger FIRE number.

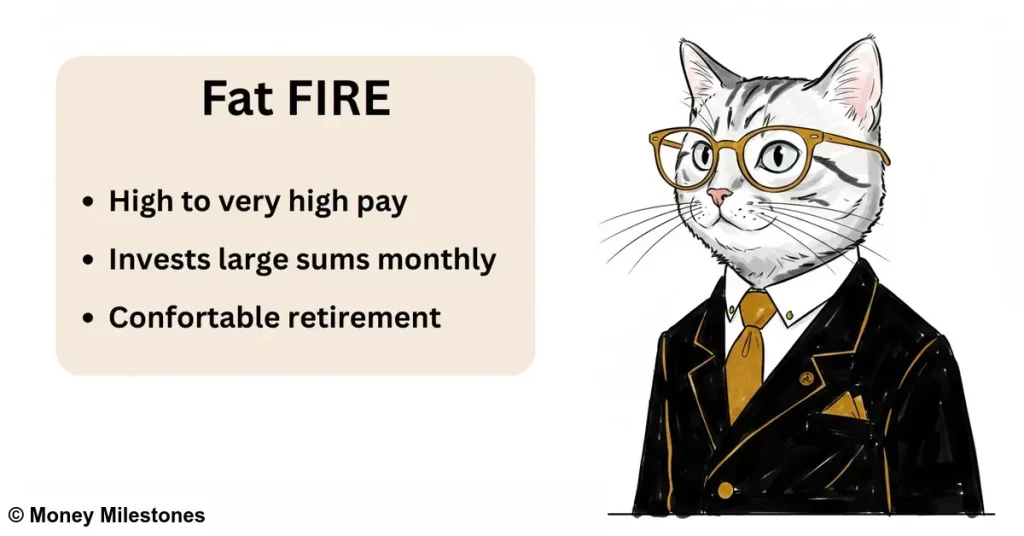

Fat FIRE: How to retire early with a high income and a comfortable lifestyle

At the opposite end of the spectrum are Fat FIRE followers. They reject frugality but make up for it by earning high (or even very high) salaries. Their spending tends to be more relaxed, but they can still maintain average or high savings rates thanks to their income. Because they plan for a comfortable retirement, their FIRE number is also high. But with strong earnings, they can still reach it relatively quickly.

How to retire early: A fat FIRE example

Let’s illustrate the concept of Fat FIRE with an example. Sujata, 30, is a senior software engineer at a large tech company. Her take-home pay is £8,500 per month, including bonuses. She holidays in Spain twice a year, enjoys skiing trips in the Alps, and only buys deluxe croquettes for her dog. Despite her lifestyle, her high income allows her to save around £4,500 each month.

Sujata wants to retire with a comfortable annual income of £80,000, giving her a FIRE number of £2 million. With £150,000 already saved, and assuming a 5% annual investment return, she could retire in 18.6 years, at around age 48 or 49.

Fat FIRE is all about earning a high income, enjoying life, and still saving enough to retire early.

Is fat FIRE right for you: Pros and cons of retiring early with a high income

Fat FIRE might suit you if:

- You earn a high or very high salary. Your income gives you the freedom to spend and save at the same time.

- You have the discipline not to spend it all. Even with a big salary, you’re willing to invest a significant chunk each month.

Fat FIRE probably isn’t for you if:

- You’re on a regular salary.

- You earn a lot but also spend a lot. If your outgoings rise with your income, Fat FIRE will be out of reach.

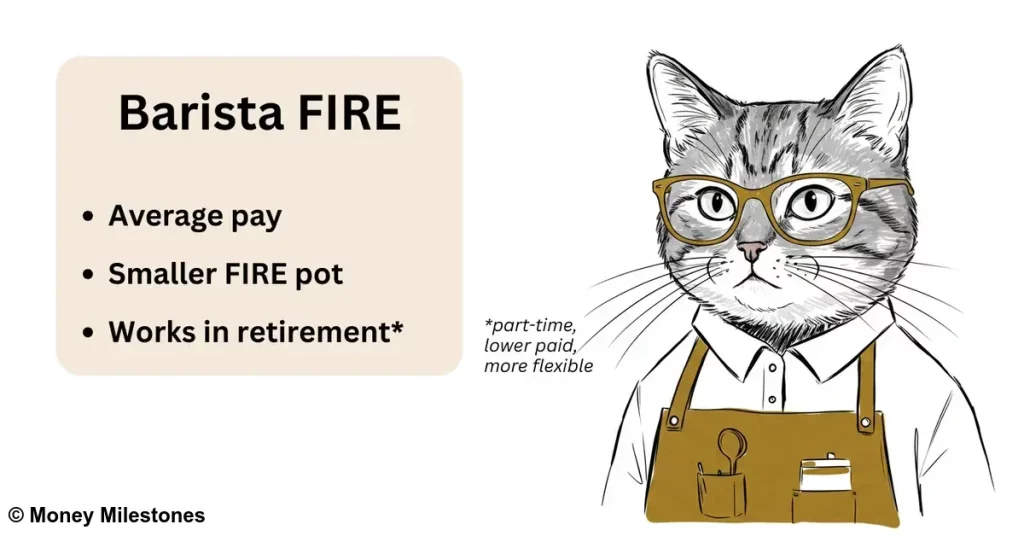

Barista FIRE: How to retire early with part-time work and flexibility

If you’re not the frugal type and don’t have a sky-high salary, there’s still another option: Barista FIRE. People pursuing Barista FIRE usually earn average salaries and live fairly frugally, though not as extremely as their Lean FIRE cousins. Their secret? They don’t plan to fully retire.

Instead, the idea is to build up a solid FIRE pot, then leave their current job and move into a different role: one that’s part-time, lower paid, more flexible, or simply more enjoyable. It could be a dream job that doesn’t pay well (like being a barista — hence the name), but it doesn’t have to be.

Because they plan to keep earning some income after leaving their main career, their FIRE number is much lower than that of someone aiming for full retirement. One extra bonus: by continuing to work, they often keep valuable employee benefits like private medical insurance, which would otherwise need to be paid out of pocket.

How to retire early: A barista FIRE example

Let’s look at Bob, a 26-year-old plumber with a salary of £33,000 and no savings. His take-home pay is £2,270 per month. Bob also loves playing the guitar and dreams of spending more time gigging and recording music. But he knows that dropping everything to become a full-time musician would be too risky. So instead, he plans to retire early from plumbing and pursue his passion for music.

Bob currently spends £1,270 each month, saving £1,000. That’s a savings rate of 44%. He believes he can make about £12,000 a year from music but wants to maintain his current lifestyle. To do this, he needs an additional £270 per month. Factoring in tax, that’s around £4,500 annually. So, his “retirement” income is much lower than someone aiming for Lean FIRE.

Bob’s FIRE number is just £112,500. With an average return of 5% on his investments, he’ll reach that number in just 7.8 years, at the age of 33 or 34. Not bad for someone just starting out!

Is barista FIRE right for you: Pros and cons of early partial retirement

Barista FIRE might suit you if:

- You have a normal to high salary. Your income allows you to save a significant portion each month.

- You’re willing to work part-time in ‘retirement’. After reaching financial independence, you’re happy to work in a job you enjoy or in a less stressful, part-time role.

- You value flexibility. You’re interested in achieving financial independence without fully retiring, allowing you to balance work and personal life on your terms.

Barista FIRE probably isn’t for you if:

- You want to fully retire. If you have no interest in working once you achieve FIRE, Barista FIRE is not the right approach for you.

4 ways to retire early: calculate your FIRE number and time to FIRE

As we’ve explored in this article, there isn’t just one way to achieve early retirement. Your path to financial freedom depends on factors like your income, how much you’re willing to save each month, and whether you’re open to working part-time after achieving FIRE.

If you want to calculate your own FIRE number and time to FIRE, you can use my early retirement calculator below. This tool, also available as a standalone calculator on Money Milestones, helps you estimate how long it will take to retire early. Simply input your current savings (FIRE pot only!), how much you’re saving monthly, your expected investment growth rate, and your target first-year retirement income.

Debt: Pay it off first for a smoother path to FIRE

There’s one more thing we need to talk about. Before focusing on building your FIRE pot, it’s important to address any high-interest debt, such as credit card debt or payday loans. The interest rates on these debts are often so high that they will likely outweigh any potential returns you might earn from investments in the short term.

By paying off this debt first, you can avoid the financial drain of interest payments and build a stronger foundation for your journey to financial independence. If you’re struggling with debt, you can reach out to the National Debtline, a free and confidential service.

If you found this article helpful, why not explore some of my other posts on Money Milestones? I’ve got plenty more tips to help you take charge of your financial future, like my ultimate emergency fund guide or my article on how to negotiate a pay rise.

Note: We’ve ignored the impact of the State Pension in this article to keep things simple.